May 19, 2023

download a capital call template

Private equity firms’ dry powder, aka the uncalled capital committed by investors at the outset of their joining a private equity fund or a venture capital (VC) fund, continues to hit new records. So how do these levels come down? Fund managers in the private equity and VC spaces must “call” this capital once they’re ready to put it to use.

In these situations, fund accounting teams must kick off capital calls, influencing the cash flow of the investment fund. Let’s get into the specifics.

DOWNLOAD OUR PRIVATE EQUITY REPORTING PACKAGE

What is a capital call?

Private equity capital call definition

A capital call, whether in the private equity or venture capital space, is the act of a fund manager requesting a certain amount of committed capital from investors once the manager needs it, such as when the fund has identified an attractive investment opportunity it would like to act on. Investors are alerted via a private equity report called a capital call notice and have a deadline to transfer this capital to the investment fund, at which point it becomes “paid-in capital”.

When investors, or limited partners, sign onto a PE or VC fund and commit to a certain level of investment, their limited partner agreement (or LPA) dictates their upfront capital contribution, as well as other stipulations such as carried interest and fund duration. The original investment amount less the capital provided up front is their uncalled capital, and represents the amount of money that can be subject to capital calls at any time over the life of the fund, with specific stipulations around volume and frequency laid out in the LPA.

INFOGRAPHIC: Complete a Capital Call in 10 Minutes

What happens if private equity investors don’t meet their obligations for capital calls?

Penalties for investors who have defaulted and are unable to pay a capital call by the deadline would differ depending on the PE or VC fund, with specific actions laid out in the LPA. Common next steps could include:

- Accruing interest on the missing capital

- Initiating legal proceedings

- Offering up purchase of the defaulted investor’s share of the fund pro rata to other fund investors

- Selling the defaulted investor’s share of the fund on the secondary market

General partners’ challenges in managing capital calls

LP and regulatory reporting activities are already named as the top operating challenge by 70% of general partners, per Allvue data. Without the right engine powering a private equity or VC fund’s end-to-end operations, managing capital calls requires plenty of time, attention, and resources.

Depending on the size of a private equity or venture capital fund, there may be anywhere from dozens to hundreds of investors, each with varying share sizes in the fund – thus each of those investors needs its own capital call investor report generated. Unless the investment fund has the right tools to automatically generate these notices, the process is likely to be lengthy and error prone.

Once the capital call notices are sent out, fund teams are then challenged to keep track of numerous incoming wires and accurately pairing them with each investor in order to have a correct outlook on the fund’s cash flow.

From beginning to end, the capital call process requires clear and easy access to investor data and the ability to carry those figures through as capital call notices are generated, sent out, and as additional capital is received. Without the right workflow in place, general partners will encounter chaos, and likely during a high-pressure time when they’re working against the clock to secure the capital to close an important investment deal.

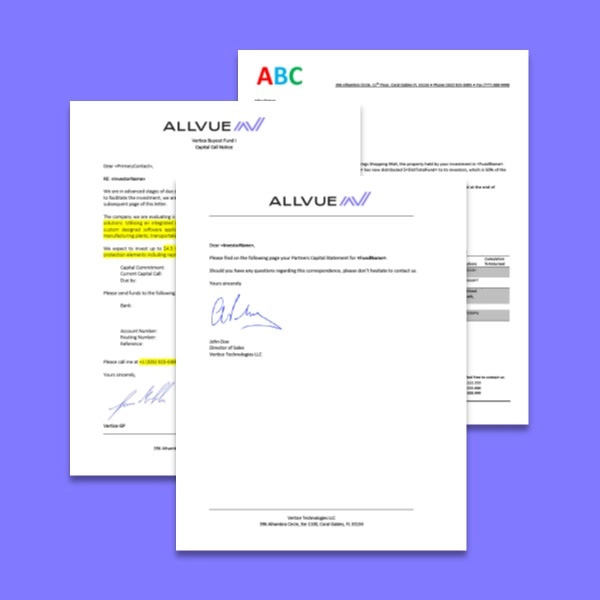

What does a capital call notice look like?

The typical private equity or venture capital capital call begins with a letter to the investor including brief details about the purpose of the capital call and the entity the fund is looking at acquiring – such as deal stage, company background, and planned acquisition cost.

The notice then lays out the individual investor’s

- Total capital commitment over the investment fund lifetime

- Call amount for this specific capital call

- Deadline for receiving the additional capital for this specific call

- Bank, account, and wire details

Following this section, investors should see a full ILPA capital call and distribution template, which goes into deeper detail as to the investor’s full commitment, contributions, distributions, and more.

To see what a typical capital call notice looks like, download our template below.

How Allvue can ease the private equity capital call process

At Allvue, we understand the complexities fund managers face in the private equity and venture capital sectors when it comes to handling capital calls and other investor communications. Our cloud-based fund accounting software has been designed with a single goal: to simplify your process, save time, and enhance accuracy.

- Efficient Capital Call Notices: Our software enables swift and accurate creation of capital call notices, complete with all necessary details including a full ILPA template.

- Track and Manage with Ease: Allvue’s Fund Accounting software includes features for the efficient management of capital calls, ensuring you have a clear perspective of your fund’s cash flow.

- Automated Reporting: Say goodbye to lengthy report creation. Our system automates capital call reports and comprehensive financial statements, bringing all vital data at your fingertips.

- Seamless Integration and Compliance: Our software is designed to integrate with your existing systems smoothly, ensuring the effortless flow of data. Rest assured, our software adheres to regulatory requirements, providing you with a secure platform.

- Effective Risk Management: Our software grants you real-time access to investment data, empowering you to mitigate potential risks effectively.

Simply put, Allvue’s fund accounting software is a solution designed to alleviate your administrative load, enabling you to direct your attention towards making profitable investments.

To see how Allvue can revolutionize your handling of capital calls:

For more information, you can:

Access the full report